Published - 5 months ago | 7 min read

Insurance Industry Tech Challenges in 2026: 3 Silent Growth Killers

The insurance sector is currently navigating a pivotal transition. The rapid acceleration of the data economy means insurers must be more innovative and agile than ever before. However, growth is currently stifled by three massive hurdles: escalating cybersecurity threats, paralyzing legacy infrastructure, and an increasingly complex regulatory landscape. These constitute the core insurance industry tech challenges of the modern era.

Digital-first "Insurtechs" are no longer just disruptors; they are existential threats posing significant competition to traditional firms. If legacy insurers fail to meet the digital expectations of modern customers—specifically the 73% of young consumers who now trust tech giants more than financial institutions—they risk irrelevance.

This guide is for CIOs, Risk Officers, and Digital Transformation Leaders. It moves beyond surface-level observations to provide an engineering-grade analysis of the most pressing insurance digital transformation challenges, including:

The Threat Vector: Why ransomware in financial services has surged by 64% and how encryption is becoming the primary weapon.

The Infrastructure Gap: How legacy systems drain IT budgets and create a "trust deficit" with digital natives.

The Regulatory Deadline: Navigating the critical resilience mandates from the UK's PRA/FCA and the EU's DORA.

The Architecture: How to implement hybrid IT and phased modernization to survive these insurance industry tech challenges.

Digital-first "Insurtechs" are no longer just disruptors; they are existential threats posing significant competition to traditional firms. If legacy insurers fail to meet the digital expectations of modern customers—specifically the 73% of young consumers who now trust tech giants more than financial institutions—they risk irrelevance.

This guide is for CIOs, Risk Officers, and Digital Transformation Leaders. It moves beyond surface-level observations to provide an engineering-grade analysis of the most pressing insurance digital transformation challenges, including:

The Threat Vector: Why ransomware in financial services has surged by 64% and how encryption is becoming the primary weapon.

The Infrastructure Gap: How legacy systems drain IT budgets and create a "trust deficit" with digital natives.

The Regulatory Deadline: Navigating the critical resilience mandates from the UK's PRA/FCA and the EU's DORA.

The Architecture: How to implement hybrid IT and phased modernization to survive these insurance industry tech challenges.

The Cybersecurity Crisis: Securing Insurance Digital Transformation

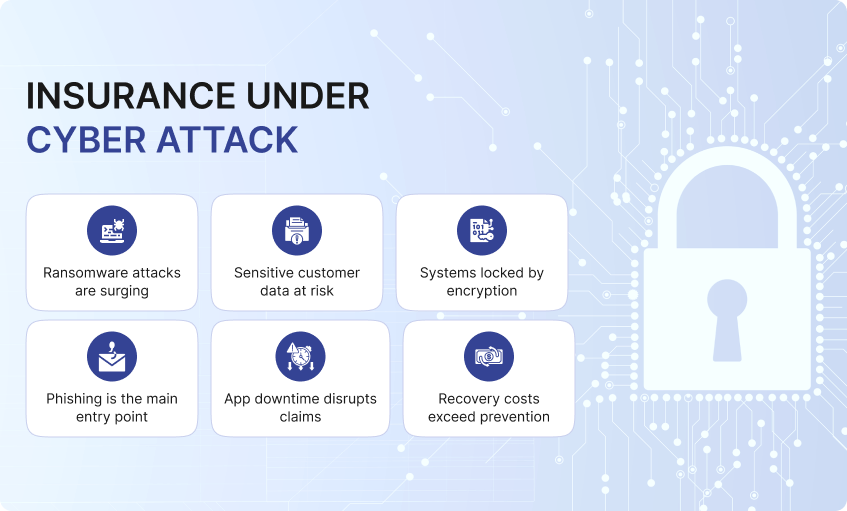

As insurance companies undergo rapid insurance digital transformation, they inevitably collect, store, and process massive volumes of sensitive data. This data gravity makes them prime targets. Among all insurance industry tech challenges, cybersecurity is the most immediate threat to operational continuity. The challenge is no longer just about preventing entry; it is about maintaining operational resilience under siege.

The Quantifiable Rise in Threat Vectors

The financial services sector is facing a targeted onslaught. Recent industry data indicates a staggering 64% increase in ransomware attacks targeting this sector. Even more concerning is the efficacy of these attacks: 81% result in successful data encryption, locking firms out of their own critical infrastructure.

According to the government data, 50% of UK businesses have already suffered some form of cybersecurity breach. The cost of these incidents is twofold: there are the direct damages of the breach, but often, the cost of recovery exceeds the cost of implementing new systems entirely. This financial strain is one of the most debilitating insurance digital transformation challenges facing CFOs today.

According to the government data, 50% of UK businesses have already suffered some form of cybersecurity breach. The cost of these incidents is twofold: there are the direct damages of the breach, but often, the cost of recovery exceeds the cost of implementing new systems entirely. This financial strain is one of the most debilitating insurance digital transformation challenges facing CFOs today.

Deconstructing the Attack Surface

Cybercriminals are evolving their tactics to exploit specific vulnerabilities in the insurance workflow. Addressing these cybersecurity risks in insurance requires understanding the specific vectors:

Phishing at Scale: This remains the most pervasive form of cyberattack. Attackers trick employees into clicking links in seemingly harmless emails, bypassing firewalls by exploiting human error.

DDoS Attacks: Criminals are increasingly overloading insurance servers to cause slowdowns or complete unavailability of apps. For an industry reliant on 24/7 claims processing, downtime is a revenue killer.

Physical Vector Risks: The use of infected removable media (USB drives) to bridge air-gapped systems remains a critical, often overlooked threat.

Malware Deployment: Malicious software is frequently deployed to gain silent network access, allowing attackers to steal data over months before detection.

Phishing at Scale: This remains the most pervasive form of cyberattack. Attackers trick employees into clicking links in seemingly harmless emails, bypassing firewalls by exploiting human error.

DDoS Attacks: Criminals are increasingly overloading insurance servers to cause slowdowns or complete unavailability of apps. For an industry reliant on 24/7 claims processing, downtime is a revenue killer.

Physical Vector Risks: The use of infected removable media (USB drives) to bridge air-gapped systems remains a critical, often overlooked threat.

Malware Deployment: Malicious software is frequently deployed to gain silent network access, allowing attackers to steal data over months before detection.

The Mitigation Strategy: From Defense to Resilience

To solve these insurance tech challenges, a modern cybersecurity posture requires shifting from "blocking" to "resilience."

Endpoint Detection and Response (EDR): EDR solutions have become mandatory defensive technologies. However, the tools alone are insufficient; proper deployment and real-time management are critical to detecting emerging threats before they escalate.

The Backup Imperative: In a ransomware environment, backups are your only insurance policy. Encouragingly, 58% of organizations that suffered attacks recently had more mature backup systems than in previous years, and the percentage of organizations with viable backups increased by 10% in 2023.

Hybrid IT Security: Implementing hybrid IT with secure colocation provides a physical and digital fortress. It allows insurers to enforce granular access controls and protect data off-premise, ensuring business continuity even if the headquarters is compromised.

Endpoint Detection and Response (EDR): EDR solutions have become mandatory defensive technologies. However, the tools alone are insufficient; proper deployment and real-time management are critical to detecting emerging threats before they escalate.

The Backup Imperative: In a ransomware environment, backups are your only insurance policy. Encouragingly, 58% of organizations that suffered attacks recently had more mature backup systems than in previous years, and the percentage of organizations with viable backups increased by 10% in 2023.

Hybrid IT Security: Implementing hybrid IT with secure colocation provides a physical and digital fortress. It allows insurers to enforce granular access controls and protect data off-premise, ensuring business continuity even if the headquarters is compromised.

The "Legacy Trap": Losing Ground to Insurtech Competition

One of the most significant barriers to growth is the reliance on legacy systems. These outdated frameworks are often incompatible with the modern technologies—such as AI, blockchain, and cloud computing—that are necessary to scale. Navigating the migration from old to new is arguably the most complex of all insurance tech challenges, primarily because it leaves traditional firms vulnerable to agile Insurtech competition.

The "Maintenance vs. Innovation" Budget War

Legacy systems in insurance act as a massive drain on resources. The vast majority of IT budgets in traditional insurance firms are spent simply on maintaining systems that are no longer fit for purpose. This creates a vicious cycle common to many insurance industry tech challenges:

1. Firms are forced to constantly patch old systems to keep the lights on.

2. This increases operational costs and accumulates technical debt.

3. Because the budget is consumed by maintenance, there is no capital left for innovation.

4. Updates to these systems to meet new market or regulatory requirements become costly and time-consuming.

1. Firms are forced to constantly patch old systems to keep the lights on.

2. This increases operational costs and accumulates technical debt.

3. Because the budget is consumed by maintenance, there is no capital left for innovation.

4. Updates to these systems to meet new market or regulatory requirements become costly and time-consuming.

The Trust Deficit: Brand vs. Experience

While traditional insurers possess strong brand equity with older generations, they face a crisis of trust with digital natives. A study by The Investment Association reveals a startling shift: 73% of young consumers trust technology companies like Google, Apple, and Amazon more than their own bank or insurer when seeking financial advice.

Trust in 2025 is a function of user experience. How much can a customer trust an insurance company if they are forced to use a clunky, slow interface to input sensitive claims data? To overcome these insurance digital transformation challenges, insurers must deliver the seamless, personalized experiences that users expect from Big Tech.

Trust in 2025 is a function of user experience. How much can a customer trust an insurance company if they are forced to use a clunky, slow interface to input sensitive claims data? To overcome these insurance digital transformation challenges, insurers must deliver the seamless, personalized experiences that users expect from Big Tech.

The Insurtech Competitive Advantage

Digital-first competitors do not carry the baggage of legacy systems in insurance. This allows them to execute on four key advantages that traditional firms struggle to match:

Faster Onboarding: They can approve new customers in minutes, not days.

Unified Customer View: They operate on a single database covering all products. This allows for instant query resolution, whereas traditional firms often rely on siloed, disconnected systems for different products.

Automated Broker Management: Digital-first systems streamline broker interactions, significantly increasing operational efficiency.

AI Integration: They natively use AI to enhance customer satisfaction and reduce operating costs, rather than trying to bolt it onto a mainframe from the 1990s.

Faster Onboarding: They can approve new customers in minutes, not days.

Unified Customer View: They operate on a single database covering all products. This allows for instant query resolution, whereas traditional firms often rely on siloed, disconnected systems for different products.

Automated Broker Management: Digital-first systems streamline broker interactions, significantly increasing operational efficiency.

AI Integration: They natively use AI to enhance customer satisfaction and reduce operating costs, rather than trying to bolt it onto a mainframe from the 1990s.

Operational Resilience Compliance: DORA, GDPR, and the New Liability

Rapid digitalization often outpaces regulatory frameworks, making compliance a moving target. Operational resilience compliance is no longer just about filling out forms; it is about building technical resilience. As 2025 approaches, compliance has become one of the most urgent insurance digital transformation challenges.

The UK Mandate: PRA and FCA Operational Resilience

The Prudential Regulation Authority (PRA) and Financial Conduct Authority (FCA) have introduced comprehensive regulations that fundamentally change how firms must view disruption. This is not just a checkbox exercise; it is about protecting the integrity of the UK financial system.

The Timeline: 31 March 2025 By this date, all firms must have completed comprehensive mapping and testing to ensure they can operate within their "impact tolerances".

Identify Important Business Services: Firms must categorize which services, if disrupted, would cause harm to consumers.

Set Impact Tolerances: You must define the maximum acceptable level of disruption for each service.

Third-Party Oversight: Starting 1 January 2025, the Bank of England and FCA enforced oversight of critical third-party providers. You could no longer outsource your liability for the insurance industry.

The Timeline: 31 March 2025 By this date, all firms must have completed comprehensive mapping and testing to ensure they can operate within their "impact tolerances".

Identify Important Business Services: Firms must categorize which services, if disrupted, would cause harm to consumers.

Set Impact Tolerances: You must define the maximum acceptable level of disruption for each service.

Third-Party Oversight: Starting 1 January 2025, the Bank of England and FCA enforced oversight of critical third-party providers. You could no longer outsource your liability for the insurance industry.

The EU Mandate: Digital Operational Resilience Act (DORA)

Similarly, the EU's DORA regulation becomes effective in 2025. It raises the stakes significantly by placing responsibility for compliance directly on the management body.

Board-Level Accountability: Compliance is no longer just an IT problem; boards, executive leaders, and senior stakeholders are personally accountable.

ICT Incident Liability: DORA holds insurance companies—and their main third-party providers—accountable for ICT incidents.

Severe Penalties: Non-compliance can result in significant fines, sanctions, and even criminal proceedings for company directors, depending on the jurisdiction.

Board-Level Accountability: Compliance is no longer just an IT problem; boards, executive leaders, and senior stakeholders are personally accountable.

ICT Incident Liability: DORA holds insurance companies—and their main third-party providers—accountable for ICT incidents.

Severe Penalties: Non-compliance can result in significant fines, sanctions, and even criminal proceedings for company directors, depending on the jurisdiction.

The Technical Compliance Response

To survive this scrutiny and solve these insurance digital transformation challenges, insurers must integrate compliance into daily technical operations:

Automated Compliance Checks: Implementing solutions to automate reporting streamlines the process, though human oversight remains necessary.

Real-Time Monitoring: Tools must be deployed to monitor regulatory changes in real-time.

AI-Driven Analysis: AI tools can reduce operational overheads by analyzing vast volumes of regulatory data and generating automated reports, effectively mitigating the risks associated with insurance regulatory compliance.

Automated Compliance Checks: Implementing solutions to automate reporting streamlines the process, though human oversight remains necessary.

Real-Time Monitoring: Tools must be deployed to monitor regulatory changes in real-time.

AI-Driven Analysis: AI tools can reduce operational overheads by analyzing vast volumes of regulatory data and generating automated reports, effectively mitigating the risks associated with insurance regulatory compliance.

The Solution Stack: Architecting for Resilience

Solving these insurance tech challenges requires a strategic shift from "maintenance" to "modernization." Insurers must stop patching the old and start building the new.

The Migration Strategy: Big Bang vs. Phased

Insurers often fear transformation because it seems overwhelming. There are two distinct architectural paths to modernization when facing insurance industry tech challenges:

Option A: The Big-Bang Approach

The Logic: Transform all systems in one go.

The Pros: Offers a "clean slate" and immediately removes technical debt.

The Cons: Extremely risky. High probability of operational disruption during the switchover.

Option B: Phased Transformation (Recommended)

The Logic: Take a system-by-system approach.

The Pros: Less disruptive to daily operations. Allows for "course correction" during the journey.

The Cons: Takes longer to fully execute.

The Verdict: For most established firms, a phased approach leveraging hybrid infrastructure helps manage the transition while minimizing the risk of exacerbating existing insurance industry tech challenges.

Option A: The Big-Bang Approach

The Logic: Transform all systems in one go.

The Pros: Offers a "clean slate" and immediately removes technical debt.

The Cons: Extremely risky. High probability of operational disruption during the switchover.

Option B: Phased Transformation (Recommended)

The Logic: Take a system-by-system approach.

The Pros: Less disruptive to daily operations. Allows for "course correction" during the journey.

The Cons: Takes longer to fully execute.

The Verdict: For most established firms, a phased approach leveraging hybrid infrastructure helps manage the transition while minimizing the risk of exacerbating existing insurance industry tech challenges.

Partnering for Scale

Insurance companies do not have to approach this alone. Partnering with a data center provider with a global footprint allows you to "borrow" their scale and security.

Secure Connectivity: A partner can provide the secure, performant connectivity needed to support granular access controls.

Compliance-Ready Infrastructure: Leveraging colocation facilities that are already compliant with DORA/GDPR standards removes a massive burden from your internal team, allowing you to focus on other insurance industry tech challenges.

Secure Connectivity: A partner can provide the secure, performant connectivity needed to support granular access controls.

Compliance-Ready Infrastructure: Leveraging colocation facilities that are already compliant with DORA/GDPR standards removes a massive burden from your internal team, allowing you to focus on other insurance industry tech challenges.

Conclusion: From Fragile to Resilient

The absence of solutions to these three challenges will inevitably lead to regulatory fines, loss of customer trust, and increased operational costs. The legacy "patch-and-pray" method is no longer viable in a world where insurance industry tech challenges define the difference between growth and bankruptcy. However, by proactively addressing cybersecurity risks in insurance, retiring the debt of legacy systems in insurance, and automating insurance regulatory compliance, companies can establish a technology infrastructure that does more than just survive, it accelerates growth. The future belongs to those who treat these insurance tech challenges not as IT problems, but as strategic business imperatives. The deadline is 2025. The time to architect your defense is now.

Written by / Author

Manasi Maheshwari

Found this useful? Share With

Top blogs

Most Read Blogs

Wits Innovation Lab is where creativity and innovation flourish. We provide the tools you need to come up with innovative solutions for today's businesses, big or small.

© 2026 Wits Innovation Lab, All rights reserved

Crafted in-house by WIL’s talented minds